The Internal Revenue Service (IRS) recognizes as ministers those who are credentialed by a religious body, have authority to conduct religious functions, and are currently recognized as religious leaders by the church organization they are serving. For more information, see IRS Publication 517.

When a person’s circumstances fit the IRS criteria, the person is to be treated as a minister for tax purposes. This status is not to be changed (either to minister status or to non-minister status) for economic or preference reasons. Where the facts support the minister status, the following tax rules apply:

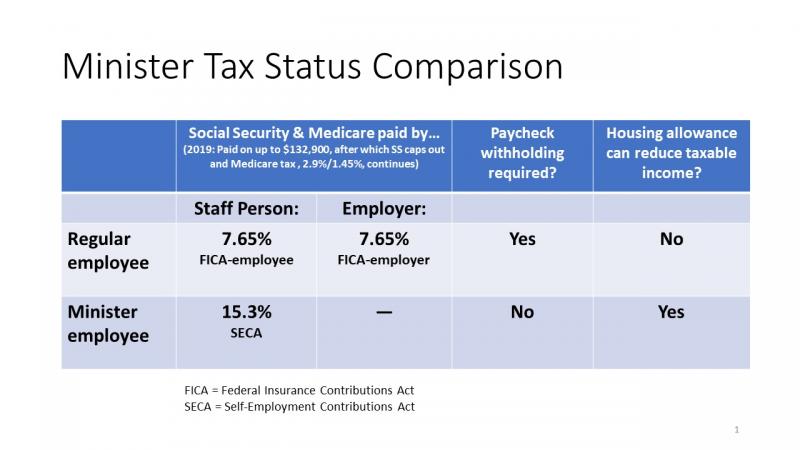

1. Dual status – The minister is an employee for income tax purposes and should receive a W-2 from the church. The minister is not a “contract” or 1099 worker unless meeting the full definition of self-employed (such as a consultant providing services to multiple organizations). But the minister is considered “self-employed” for Social Security purposes, which means …

2. SECA tax – The minister must pay the Self Employed Contributions Act (SECA) rate for Social Security and Medicare tax; this rate is equal to the combined employee and employer FICA rates. The church/employer should not withhold employee FICA or contribute employer FICA. This payment is the responsibility of the minister.

3. Tax withholding not required – While the minister must pay the applicable taxes, withholding of those taxes from pay is not required. The minister may file quarterly estimated taxes or may request that the employer withhold and remit a dollar amount that the minister specifies. It is up to the minister to estimate tax liability and ensure that a sufficient amount – covering both income tax and SECA tax – is submitted timely. Any voluntary withholding is remitted to the IRS simply as income tax payment. The breakdown between income tax and SECA tax is determined with the filing of the minister’s 1040 tax return that must include the SE form.

4. Eligible for housing allowance – The minister may exclude designated housing allowance expenses from income when properly determined according to IRS guidelines. The housing allowance is not excluded from compensation for purposes of SECA tax, however.

These tax rules are not separable and must all apply to treatment of the minister. (e.g. The employer cannot contribute/withhold FICA and also designate housing allowance.)

It has been the practice of many churches, in recognition of the minister’s liability for the SECA rate and the church’s avoidance of employer FICA contribution, to pay an amount equivalent to employer FICA to the minister as additional (taxable) salary to offset the impact of the double rate. I strongly recommend such practice, since the lack of such provision actually reduces the effective salary of the minister as compared to regular employment.

For more information about ministers’ tax status, download the booklet Ministers' Tax & Financial Guide at “Tax Books Available for Download”. If you're new to minister tax treatment, you may find this narrated tutorial helpful.