The “Housing Allowance” provision in the IRS tax code can represent a significant tax-reduction benefit for ministers when implemented properly.

History

First enacted by Congress in 1921, when most churches provided a parsonage (or “manse”) to the pastor, the exclusion from taxable income was instituted so the federal government would not get involved in examining the practice of churches in providing housing to their ministers. 1954 revisions to the tax code included an equalizing treatment for ministers who provided their own housing through the method of a church designating an appropriate portion of the pastor’s compensation as housing allowance which would then not be considered taxable income.

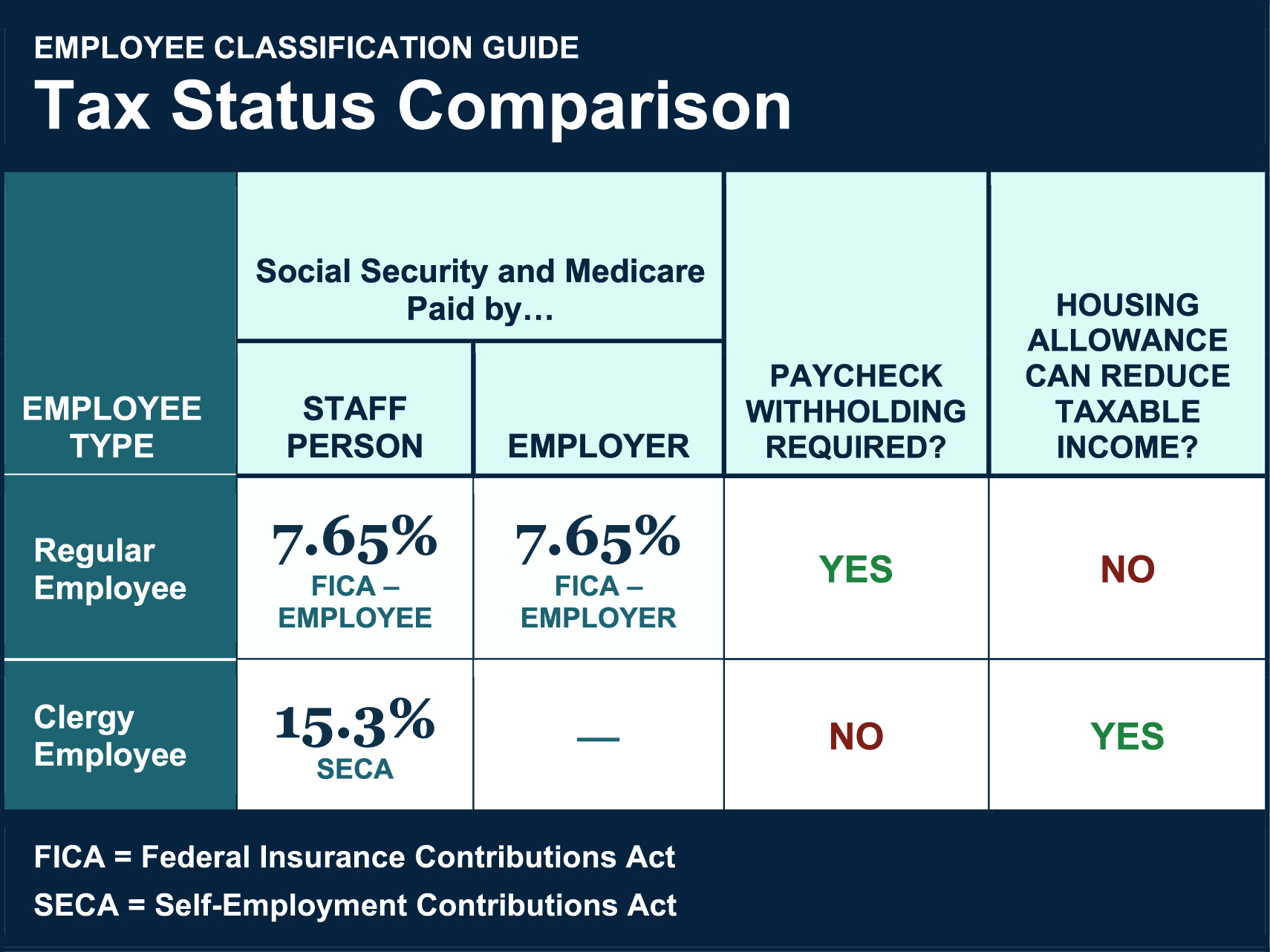

Today, qualified ministers may utilize this benefit. However, another aspect of minister status can reduce or outweigh the housing allowance exclusion because of the classification of the minister as “self-employed” for Social Security purposes, triggering a higher rate. See SECA discussion below.

Qualifying as a Minister

IRS Publication 517 defines ministers as “individuals who are duly ordained, commissioned, or licensed by a religious body constituting a church or church denomination. Ministers have the authority to conduct religious worship, perform sacerdotal functions, and administer ordinances or sacraments according to the prescribed tenets and practices of that church or denomination.” Because of the variance of church government and polity, the IRS does not address the credentialing details but does describe some criteria in Publication 517.

I would summarize the guidance as these factors:

1. The person must be credentialed as clergy (i.e. ordained, commissioned, or licensed), and

2. Meet a “balancing test” of the following factors:

- Have authority to conduct religious worship.

- Have authority to perform “sacerdotal” functions.

- Have authority to administer ordinances/sacraments.

- Have management responsibilities in the local church or denomination.

- Be considered to be a religious leader by the church or denomination.

Discussion of credentialing is beyond this article, but when a church is affiliated with a denomination that practices credentialing, the IRS will likely see more credence in the denominational credential and may see a local credential (i.e. specific to a congregation) as less certain.

In any event, clergy credentials should never be granted for the purpose of tax benefits.

The special tax rules for ministers include:

- Exclusion of a provided parsonage, or the minister’s expense of providing housing, from taxable income

- Self-employed status for Social Security tax (requiring payment of the self-employed “SECA” rate).

- Exemption from mandatory withholding. The minister is still responsible for timely paying the tax.

If a staff member meets the criteria for minister, the IRS requires the employing church to handle the compensation in this way. IMPORTANT TO NOTE: The tax aspects of minister status are not separable (exemption from withholding, self-employment income subject to SECA tax, provision for housing allowance exclusion – ALL occur together). If a person meets the criteria for minister, the IRS indicates the person must be treated that way for tax purposes. This is not a status that can be a matter of preference, by either the church or the minister.

Benefit of Minister Housing Allowance

What is it?

The exclusion from gross income for income tax purposes (but not exclusion from SE tax) of the amount used to provide a home, limited to the smallest of:

- The amount actually used to provide a home, substantiated by documented eligible expenses. (Such documentation is not submitted with a tax return but should be kept in case a tax return is audited.)

- The amount officially designated before payment of compensation (i.e. in advance by the church governing body).

- The fair rental value of the home, including furnishings and utilities.

What may be included in total of actual expenses?

All appropriate expenses related to providing a principal residence (only) are eligible, including mortgage payments, rent, utilities, repairs, furnishings, property insurance, property taxes, maintenance, improvements, and homeowner association dues.

What if the minister lives in a church-provided parsonage?

The rental value of the parsonage is not included in reportable income (W-2, Box 1) but the annual value must be added to income for calculating SECA tax, reported via Schedule C and Schedule SE on the individual’s tax return. If the minister pays utilities or maintenance, that amount may be designated in advance by the church as housing allowance. The parsonage rental value and the designated housing allowance together are added to income for determining SECA.

Similarly, the amount of the designated housing allowance for ministers providing their own housing is reported via Schedule C and Schedule SE for the purpose of determining SECA tax.

Is the housing allowance reportable to the IRS?

While some ministries include the designated housing allowance in Box 14 of the W-2 as a courtesy to the minister, data in Box 14 is informational to the employee and not required.

More about SECA Tax

For employees other than ministers, the employer must pay the employer’s share of FICA tax for Social Security and Medicare (7.65%), and must deduct the employee’s share of 7.65% from pay up to certain limits.

For ministers, the employer does not pay FICA or deduct FICA. The minister is responsible for SECA (Self Employment Contributions Act) tax instead.

NOTE: When structuring equitable pay for ministers, I believe a best practice is for the church to pay the equivalent of employer FICA to the minister so that half of the SECA tax incurred by the minister is covered. The 7.65% paid to the minister is simply taxable income, but should be considered an employer benefit and not part of the salary base. (Just as employer FICA is not considered part of a non-minister’s base salary.)